Upcoming Event

Free Newsletter

Free Newsletter

The Macroeconomics of Housing: Stop Scapegoating Cities & Towns for the Housing Crisis – It’s the Economy St—-!

By Nick Ponder, Guest Commentary //February 27, 2025//

AZ Framing and Remodeling framers work on the roof of a home under construction in Mesa on Nov. 8, 2021. (Photo by Alexandra Buxbaum/Sipa USA)(Sipa via AP Images)

The Macroeconomics of Housing: Stop Scapegoating Cities & Towns for the Housing Crisis – It’s the Economy St—-!

By Nick Ponder, Guest Commentary //February 27, 2025//

A series of very unusual economic recessions (Great Recession; Covid-19 Recession) and the following expansions changed the financial model for homebuilding. Heightened costs of labor and materials, combined with some complex financial issues, led to housing price escalation in Arizona, across the nation, and across the globe to other well-developed countries.

Arizona’s cities and towns did not cause the breakdown of the financial model for housing development, nor did they cause the housing price escalation that has been realized across the globe. Local government entities also did not influence the Federal Reserve Board to make such bad decisions that led to inflation further increasing, near zero cost access to money influencing investor purchases, and the current “Golden Handcuffs” of mortgage rates below 3.0% that is restricting housing sales.

Of course, making such arguments would be either purposefully misleading, or implies a lack of knowledge or bias among the advocates.

The correct explanation is that larger-scale macroeconomic influences negatively impacted housing affordability, and that cities and towns are helping to remedy the problem. This is not an opinion, it is an economic fact.

Fixing housing affordability problems requires developers to partner with local government entities, not scapegoat the cities and towns of impacting global housing price escalation.

WHY IS THE PROBLEM NATIONAL & INTERNATIONAL?

The housing crisis is a macroeconomic issue, not a microeconomic issue. This is why blaming zoning is a misguided analysis of the origin of the crisis and solutions to the crisis.

When you look at this in a macro sense, the housing crisis is not a micro Arizona problem but rather a macro national issue and, in many cases, an international issue. In Arizona, in particular, housing remained affordable immediately before Covid but after 2020 several shocks and factors made the housing market unaffordable.

Let’s look at several variables:

- Great Recession of 2008 and subsequent slow recovery

- Post Great Recession under-building of housing after excessive overbuilding

- Growing trend of corporate ownership in housing

- COVID work from home culture allowed people to move to places with lower costs of living (AZ); we have always been growing rapidly.

- Californians moving to AZ had higher AMI to compete with Arizonans

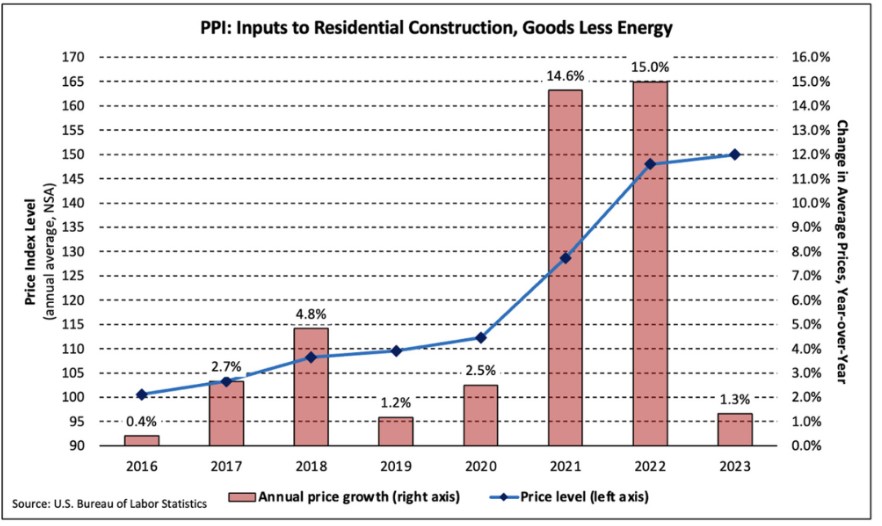

- Supply chain congestions created significant inflation in materials costs

- Changes in workforce participation inflated labor costs

- Rapid reductions followed by increases in mortgage rates by the Federal Reserve froze people in their homes

These eight variables combined with other Arizona market challenges like increasing land costs, labor costs, and regulatory challenges have pushed housing costs up by over 60%. None of these issues have to do with newly restrictive zoning! But these issues can be marginalized with better partnering between the development community and local government entities rather than the misleading and false information campaign currently being deployed by the same members of the development community.

GREAT RECESSION

Arizona was in a housing boom before the Great Recession. However, when the economy collapsed, we were hit harder and our housing industry was slower to recover. The virtual shutdown of the housing industry created a growing challenge that would be realized after Covid when several other variables came into play.

Development is on the rise. Since January 1, 2020, Arizona ranks 6th in the nation in total units permitted despite being 14th in population. We have permitted 315,000 units and constructed 249,000 of those units. Additionally, in Maricopa County alone Arizona communities have approximately 110,000 units in the pipeline and with an assured water supply certificate just awaiting construction. The 110,000 permitted units in Maricopa County are enough to satisfy today’s housing shortage.

COVID-LINKED INFLATION

The Covid pandemic created inflationary pressures in multiple ways. First, it created pressures in many individuals seeking larger homes with more space for home offices and outdoor space, inspired by greater flexibility in where they could locate as a result of telework opportunities. The beginning of the pandemic reflected a low interest rate environment that fueled competition and pushed up prices.

In addition to the initial competition created by low interest, the addition of government stimulus and the inability of people to travel or dine out inspired using disposable income on home renovations, appliances, furniture, and other products and materials used for housing.

Prior to the pandemic certain materials prices were already on the rise driven by trade disputes overseas. Those rising prices were followed by the pandemic, which saw an increased demand in all material and product areas.

One additional item often not cited is Arizona’s area median income was lower than that of California. Because of the transient nature of the new workforce, people moved from Silicon Valley and Los Angeles to Phoenix-metro during the pandemic and they brought their Silicon Valley salaries. This provided Arizonans with yet another additional challenge in an already competitive market.

INTEREST RATES

Housing is a ladder. People moving out of their starter homes and into a forever home make way for those in apartments to move into a starter home. Those moving out of a forever home and into a 55+ community make way for those moving from a starter home to scale into their forever home, and so on.

While Covid started with historically low interest rates the hot inflation that followed in 2021 was met with increased interest rates. Many Americans had already locked in at 3% interest rates. With interest rates spiking to 7% this has locked people into their homes breaking the housing ladder.

CORPORATE HOME OWNERSHIP

Since the Great Recession private equity and corporate interests have been purchasing significantly more units in the Arizona housing market. These investment opportunities diminish the supply of starter homes, competing with first-time homebuyers and increasing rents 25% or higher above their pre-sale rents.

In Phoenix-metro, 20% of the single-family rental housing units are owned by large corporate owners such as Invitation Homes (Blackstone), Tricon, Progress, and FirstKey. These entities serve as market manipulators, able to offer full cash purchases with short closing periods and no inspections; options a traditional first-time buyer cannot offer.

In addition the corporate ownership of single family homes, many communities in Arizona have been subjected to the exposure of corporate ownership in the short term rental (STR) market as well. In 2016, legislation was pursued to preempt local governments in Arizona from limiting the use of STRs in cities and towns. At the time, testimony spoke to the sharing economy and the need for the widow to rent a room in her house or the veteran to rent his home when he was deployed overseas.

Arizona became the first and only state in the country with a statewide preemption on STRs and became a testing ground for corporate ownership in the market. Today, upwards of 20% of the homes in some communities are STRs with many owned by corporations. In other communities the numbers may only be 1% to 5% but those are units that take away from individuals seeking shelter.

Today, 60,000 units in Arizona are consumed in the STR market. Further, there is a new trend in housing seeking fractional ownership of homes similar to a share in the stock market. This fractional ownership model is another way corporations keep individuals from owning homes and capitalize on the housing shortage.

Perhaps if government wants to incentivize first time individual home buying they should consider reducing the incentive for corporate ownership of individual family homes. It has often been said with worldly wisdom that if you want less of something you tax that something. Since individual homebuyers are being pushed from the market by corporate ownership entities one would consider the tax policy which treats both types of ownership identically rather than differently.

MULTIFAMILY SALES

Sales of multifamily units are at a 40-year low in the United States. Condos and townhomes are more affordable than single family homes. However, due to federal FHA regulations and, more importantly, challenges with state construction defect laws, developers are choosing to rent these units (build-to-rent) rather than sell them due to risk concerns and insurance costs, pushing sale prices higher.

Phoenix-metro has become one of the hottest markets for build-to-rent communities. Not placing these shared-wall units for sale robs Arizona first-time home buyers of a low cost options.

LAND EFFICIENCY

Arizona has limited private land. For that reason we’re are extremely efficient with the land we have. Arizona has the 3rd smallest median lot size in the nation and today, in response to limited private land, we are building smaller than we ever have.

John F Long built Maryvale and his first development averaged 9,100 sq. ft. per lot. Seventy percent of all lots in Maricopa County are smaller than his first development.

The average Maryvale lot is around 6,500 sq. ft. Today our growing communities are routinely building homes on lots smaller than the Maryvale lots of the 1950’s and 60’s.

While our communities remain committed to being efficient with the limited land Arizona has available for development, we must also create diverse options for our residents. Arizona residents want options for small, medium, and larger lots that allow them to climb the housing ladder within their same community. We need space for apartments but also lots that value the agrarian history in our communities.

Creating a one-size-fits-all option that cuts out local input and smart community planning is not what Arizona residents want.

If the State truly wants to incentivize first-time homebuyers and builders they could consider amending the State Constitution to prioritize the sale of some of the 9 million acres of the land they own for that very purpose. Providing more land for such developments would help incentivize the supply of starter homes in the State.

AGE OF OWNERSHIP & AFFORDABILITY

In recent discussions about the average age of ownership for first-time homebuyers there have been some anecdotal suggestions that in the past first- time homebuyers frequently obtained their first homes in their mid-twenties. However, data proves otherwise. While it is accurate the price have increased due to these macroeconomic forces and the age of ownership for first-time homebuyers has correspondingly increased, the average age has been over 31 years of age since 1981.

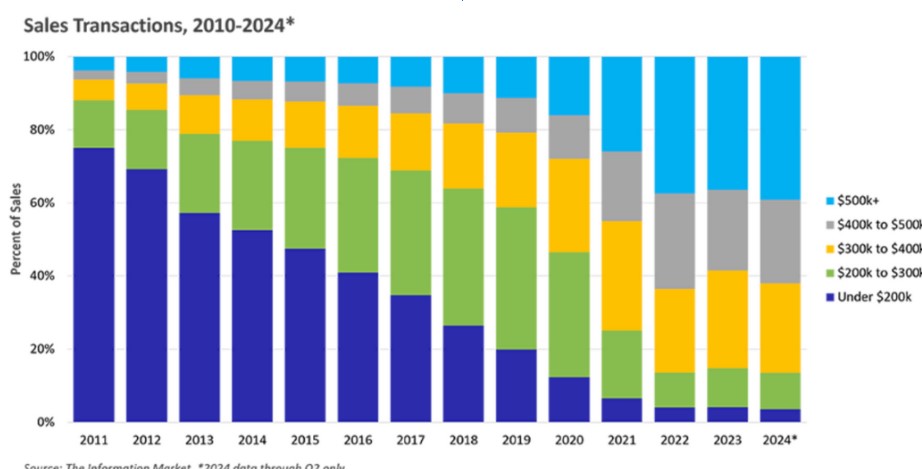

Data from the Maricopa Association of Governments, specific to the Maricopa County planning area (includes City of Maricopa, Casa Grande, Marana, Coolidge, and Florence) housing remained affordable despite the development communities under-building following the Great Recession. Through 2019 nearly 60% of all homes in the MAG region sold for under $300,000 and 80% were under $400,000.

While these market-driven forces have created the housing challenges that we have today, Arizona communities have been at the forefront of policy solutions in their communities to increase housing units. Arizona communities have reduced lot sizes, minimized setbacks, supported legislation to restrict approval timeframes, providing programs to invest locally in affordable housing, supporting the state Low Income Housing Tax Credit (LIHTC) program, and many more.

While these market-driven forces have created the housing challenges that we have today, Arizona communities have been at the forefront of policy solutions in their communities to increase housing units. Arizona communities have reduced lot sizes, minimized setbacks, supported legislation to restrict approval timeframes, providing programs to invest locally in affordable housing, supporting the state Low Income Housing Tax Credit (LIHTC) program, and many more.

Arizona municipalities, residents, and developers have built incredible, vibrant communities that are attracting businesses and people from across the globe. The answer to this point-in-time macroeconomic housing crisis is not to treat so flippantly what we’ve taken so much care, resources, and patience to curate.

We look forward to supporting more locally driven solutions to the housing challenge that keep in place the essential 3-legged stool of municipal planners, developer input, and resident input.

MYTH vs FACT

| Cities do not allow carports | Many cities allow carports and after checking with them developers have not requested to build a carport or a home w/o a garage in at least the past decade. |

| Cities have outlawed small lot homes | Cities are required by the Legislature to go through the general plan process. Lot sizes in units per acre are set forward in the general plan. We are building smaller than we ever have today. |

| Cities mandate carriage lights on homes | The city in question does not require streetlights. The $100 carriage lights take the place of thousands of dollars in streetlights. Lighting houses provides neighborhood deterrents for property crimes. |

| Cities require private streets | Cities do not require private streets. If a road is not built to spec the city will require the street to be “private” rather than conveyed to the city as it may not meet standards for public safety or public works traffic. |

| Cities require neighborhood parks as amenities, that should be the role of the city | 40 cities in Arizona do not have a primary property tax. Other cities keep property taxes very low. Those taxes are kept low by requiring, for a nominal cost in the construction of a home, small neighborhood parks rather than large taxpayer funded regional parks. |

8 QUICK TOOLS TO FIX HOUSING

Now that we have level-set the REAL reasons for the housing crisis that is macroeconomic in nature and not only hit Arizona but the nation, let’s talk about potential solutions. We believe there are 8 easy solutions to address the current housing challenges:

- Tax Increment Financing (TIF)

- Arizona is the ONLY state in the country that does not allow TIF. In many states it is used to build infrastructure which reduces taxpayer costs (impact fees) or is also used for affordable housing projects.

- Local tools (infill property tax freeze)

- In 2024 the League proposed an effort to freeze local property taxes for 7 years on infill housing projects to allow those developments to pencil out for builders.

- League Starter Home bill

- A pragmatic approach that maintains the 3-legged stool between developers, residents, and municipal planners.

- SB1698, HB2834

- Restrictions on corporate mass ownership

- SB1209

- Removing local constraints on short term rentals

- HB2308

- Extending LIHTC

- HB2660

- Correcting construction defect challenges

- We are at a 40-year low in multifamily home sales in part because of this issue.

- HB2713

- Inclusionary zoning prohibition repeal

- As part of the adaptive reuse bill from 2024, HB2297, developers were required to include 10% of the units as affordable. Some allowance for inclusionary zoning at the local level would aid in affordable and workforce housing.

- HB2595

Nick Ponder is senior vice president for Governmental Affairs at HighGround